An insuretech company launched in California today with the promise of providing online homeowners insurance quotes in 60 seconds in what the Mountain View, Calif.-based company is calling "the most fundamental redesign of home insurance in recent times."

Hippo Insurance announced its launch in California and is offering what it says is "a vastly more protective product that can be quoted and purchased instantly online and at lower prices."

It's also a product that leaves the insurance agent out of the equation.

According to a company executive, a homeowners policy can be bound in roughly three minutes.

Hippo has been raising funds for more than two years to get to this point. At the end of 2016, the firm announced it closed a $14 million Series A round led by Horizons Ventures, which invests in disruptive technology and startups. It was joined by RPM Ventures, Propel Venture Partners, GGV Capital and Pipeline Capital as well as number of FinTech investors and entrepreneurs.

The company is only operating in California now, but Hippo's stated goal is to operate nationwide.

Hippo's online web portal requires consumers to start off by typing in their address, and then Hippo's software searches a host of data providers to bring back most of the information that is traditionally asked when applying for homeowners insurance, according to Rick McCathron, Hippo's head of insurance.

"We can get the basic questions narrowed down to three simple questions," McCathron said.

According to McCathron, who noted that he's "not just a tech guy" – he holds the CPCU AND CIC designations – property-specific information is gathered through traditional and non-traditional data sources. He declined to offer specifics on those sources, stating such information is proprietary.

Visitors to the site are then asked to confirm all the information is correct, and then answer three questions pertaining to discounts, such as "Do you have a fire extinguisher," "Do you have a monitored alarm."

The quote follows immediately. If a consumer chooses to bind the insurance, another 10 underwriting questions are presented.

McCathron believes a consumer can bind a policy in three minutes.

"Everything is direct to consumer," he said.

Consumers who fall outside of the company's "underwriting box" are immediately notified, and are offered a conversation with one of the wholesalers Hippo has partnered with, according to McCathron, who declined to name Hippo's wholesaler partners.

The promise of returning a comprehensive insurance quote in a minute was a bit hard to swallow for some.

There are more than 120 customizing endorsements available for a homeowners' policy, noted Christopher J. Boggs, executive director of the Big I Virtual University for the Independent Agents and Brokers of America Inc.

"I would be amazed if any carrier, regardless of how intelligent their system, could accurately assess an insured's exposure and properly customize any policy with just 60 seconds of contact," Boggs said.

He was quick to note that he isn't knocking the insuretech's efforts to innovate.

"There are some efficiencies created by the artificial intelligence companies such as Hippo, Lemonade and others have created that I think the industry needs to adopt," Boggs said. "There are facets of what these companies have created that could greatly benefit independent agents and their clients."

However, there is a "sweet spot," which is the combining of AI with human reasoning and communication skills, he added.

"Insurance is ultimately a relationship business, and AI alone fails miserably at establishing relationships," Boggs added.

Hippo has partnered with TOPA Insurance in California to act as the carrier to back policies. Swiss RE is the reinsurer.

Hippo is considered a managing general agency. The company is the provider of the insurance products and the processing for the policyholder, and it earns a commission from the reinsurance company to provide the aspects that a traditional insurance company would provide.

McCathron declined to provide details on the commission structure.

Hippo's claims to have produced the "most fundamental redesign of home insurance in recent times" are supported by its changes to the user interface, providing enhanced products, and functioning as a proactive insurer, according to him.

Its "enhanced coverage" includes: Equipment Breakdown ($100,000); Service Line ($10,000); Workers' Comp (Included); Home Office ($8,000); Computers ($8,000); Water Backup ($10,000); Jewelry & Watches ($2,000).

McCathron said that instead of outmoded coverage on items like furs, pewter, and grave markers, Hippo has opted to offer coverage on things that may be more important to Millennials, such as home office coverage, computers and electronic equipment.

He also said the extended coverage addresses protections that policyholders probably believe they have but don't.

Service line protection, for example, provides coverage if a water break occurs on the insured's side of the home, and the equipment breakdown protection covers the HVAC system and the hot water heater.

"We believe that some 70 percent of people are not covered for things that they should be covered for or are not covered for things that they thought they were covered for," McCathron said.

The step that makes the company a proactive insurer, according to him, is providing water leak protection sensors to policyholders, which can be connected to the home Wi-Fi so anytime a leak is detected the policyholder and the insurer are instantly notified.

In a trial of the site, an address of a home in an upper middle-class area of Long Beach, Calif. was inputted.

Information including year built, square footage, roof type, construction type of home and number of stories were automatically filled in. The site asked for details on the home's fixtures and finishes: "Just the basics," "A few extras, "Top of the line."

In the trial, "A few extras" was chosen, which yielded the message "Finally, let's see if you qualify for any discounts." The options were "Recent home purchase," "Gated Community," "Homeowners' Association."

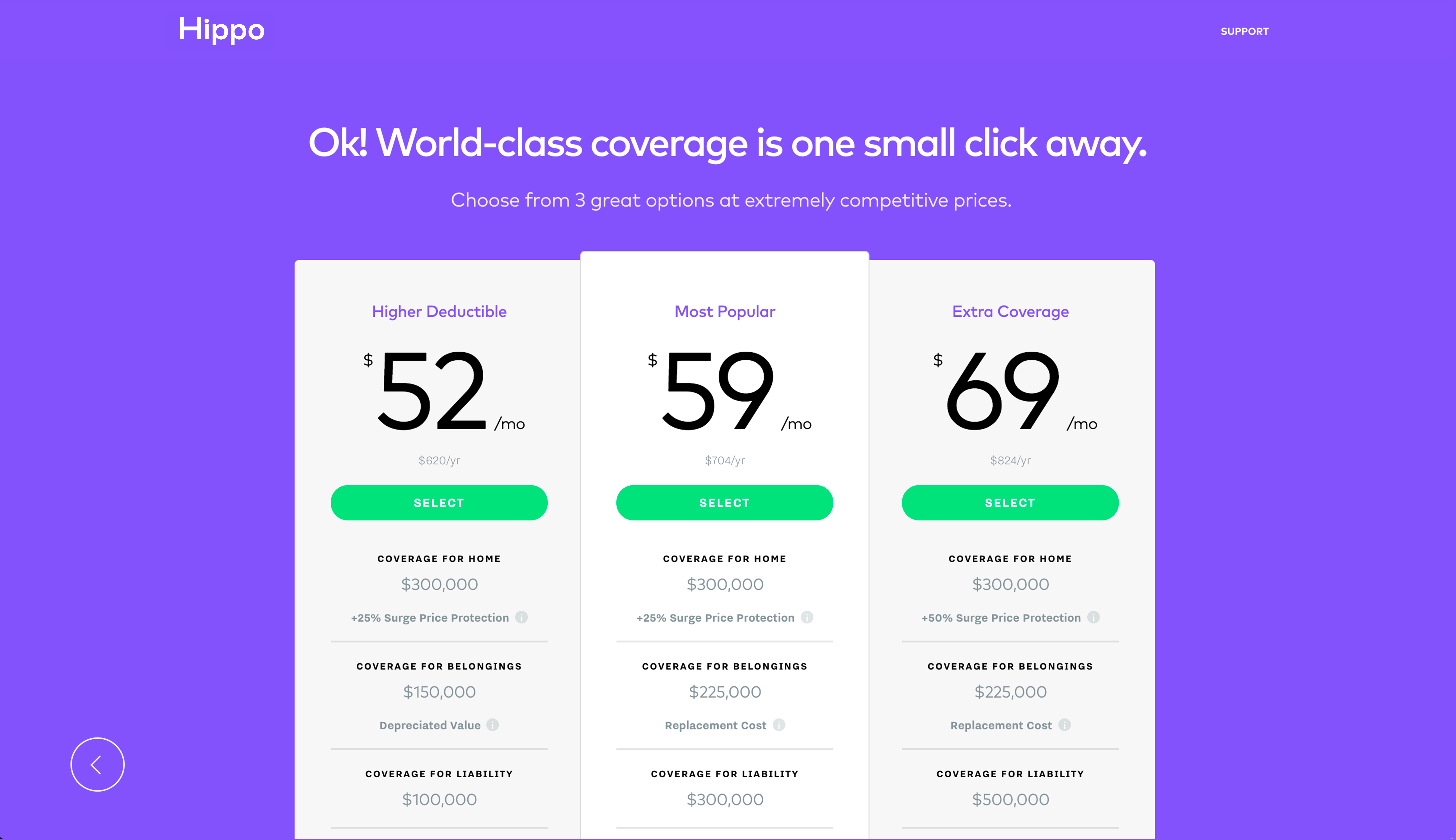

A "Recent home purchase" choice produced three options for $350,000 coverage (plus 25 percent Surge Price Protection).

A "Higher Deductible" choice was offered at $57 per month ($686 per year) for $175,000 in coverage for belongings, $100,000 coverage for liability and a $1,500 deductible. The "Most Popular" plan was $65 per month ($780 per year), with $262,500 coverage for belongings, $300,000 for liability and a $1,000 deductible. And an "Extra Coverage" plan was $76 per month ($909 per year) for $262,500 coverage for belongings, $500,000 coverage for liability and $1,000 deductible.

A page followed with choices including "Non-primary residence," "Under construction," "Secondary heat source" and "Nanny or other employee(s) on site."

Answering "No" to all returned a page with safety questions – "Central burglar alarm," "Central fire alarm," "Fire extinguisher," and "Sprinkler system."

Choosing "Central burglar alarm" and "Fire extinguisher" produced a page inquiring whether either plumbing or electrical had been updated in the last 50 years for homes built before 1967.

A "No" reply returned a page with a prompt offering a "quick chat" and a phone number because the plumbing and/or electrical was so old the process could not be completed online.

Using a back button and then answering "Yes" to both returned a page with fill-in spaces for the insured's name, date of birth, email and weather the insured already had an active homeowners policy.

Following that came a page on which the user was informed that a "quick claim check" needed to be run. The page requested the insured's primary address for the past year, and whether there had been any home claims in the last five years.

Answering "no claims" in the last five years returned a $62 per month premium ($753 per year) quote. A "checkout" page follows with options for payment frequency (annually, semi-annually or quarterly), payment method, credit card number and billing information.

California is the first of many states Hippo expects to saunter into, according to McCathron.

"We have our eye on several other states in order to facilitate a national expansion," he said. "Our ultimate goal is to be a provider of home insurance products in 50 states and we have an aggressive growth strategy to achieve that."

Comments

Add Comment